Valuation Hub

The Ultimate Guide to Stock Valuation.

Your Comprehensive Online Resource.

Welcome to the central hub for mastering stock valuation. This comprehensive online resource breaks down 8 essential methods, offering clear explanations and practical insights for serious investors to learn at their own pace.

Always free. No signup required.

Stock Intrinsic Value

Imagine a stock is like a fruit tree. The market

price you see on the ticker is the price someone is willing to pay for

the fruit right now. The intrinsic value is an estimate of how much the

tree (the company) is really worth based on how much fruit it will grow, how healthy it is, and how much it can be sold for in the future.

Stock valuation is the process of using a formula or model to calculate the intrinsic value. Remember, every model uses guesses (growth rates, discount

rates, industry multiples). The art of investing is choosing reasonable

guesses, using several models for confirmation, and staying patient while the

market eventually reflects the tree’s real value.

How Do We Find It?

Investors act like detectives. They use specific tools—called valuation models—to calculate this number. Think of these models as advanced calculators. Instead of guessing, they look at hard facts like:

- How much profit the company makes today.

- How fast the company might grow in the future.

- How much cash they have in the bank versus how much debt they owe.

The Buy or Sell Decision

Once you calculate the Intrinsic Value, you simply compare it to the Market Price (the price tag). It becomes a clear comparison:

-

Undervalued (Buy)

If your math says the Intrinsic Value is $50, but the Market Price is only $30, the stock is on sale. This is a "margin of safety" and usually a great time to buy.

-

Overvalued (Sell/Avoid)

If your math says the Intrinsic Value is $50, but the Market Price is $80, it’s overpriced. You are paying more than it's worth. It’s better to sell or wait for the price to drop.

The goal of Old School Value is to give you the tools to find that "real" number yourself, so you never overpay for a stock again.

Explore Our Stock Valuation Models

Price Multiple Valuation

Quickly compare a company's stock price to its earnings, sales, or book value against industry peers or its own history.

Learn MoreDiscounted Cash Flow (DCF)

Estimate a company's value based on its projected future cash flows, discounted back to their present value.

Learn MoreGraham Formula

A classic, conservative formula from Benjamin Graham for estimating the intrinsic value of a growth stock.

Learn MoreAbsolute P/E Model

Determine a fair P/E ratio for a company based on its growth rate, dividend payout, and market interest rates.

Learn MoreNet-Net Working Capital and Net Current Asset Value

A deep value strategy focusing on companies trading below their liquidation value, pioneered by Benjamin Graham.

Learn MoreAsset Reproduction

Value a company based on the cost to replace or reproduce its existing assets, offering a tangible floor for valuation.

Learn MoreEarning Power Value (EPV)

Focus on a company's sustainable earning power to derive its intrinsic value, assuming no future growth.

Learn MoreOwner Earnings

A Warren Buffett-inspired method that looks at the true cash flow available to owners, beyond reported net income.

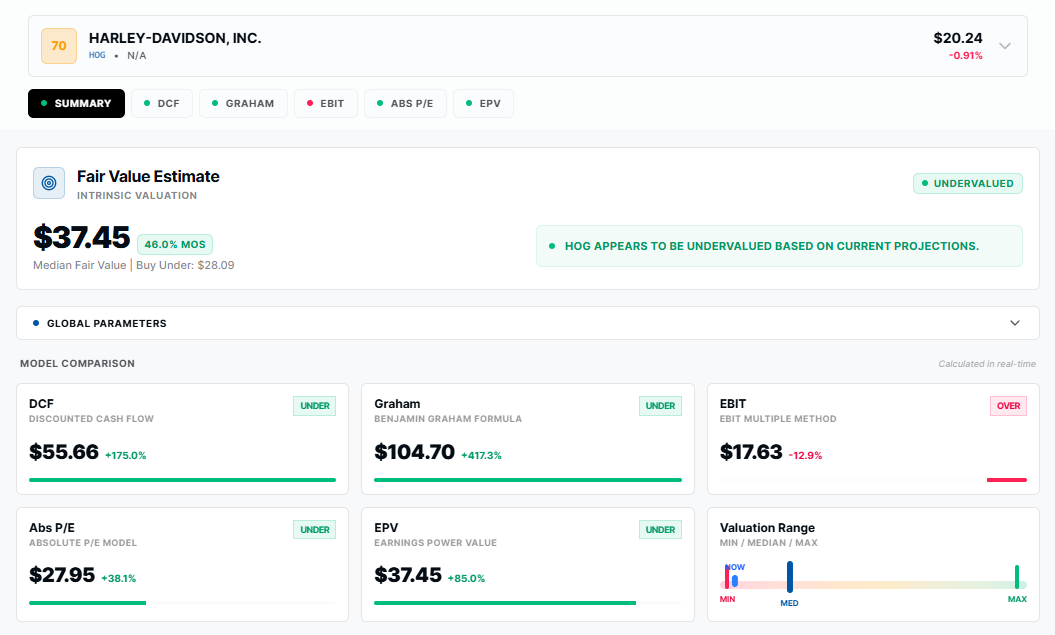

Learn MoreOld School Value Valuation Dashboard

Stop crunching numbers manually. Our dashboard automatically runs five powerful valuation models—DCF, Graham Formula, EBIT Multiples, Absolute P/E, and Earnings Power Value (EPV)—to calculate a comprehensive price target.

Fair Value Estimate

We synthesize these models into a single Fair Value Estimate, giving you a reliable baseline to compare against the current market price.

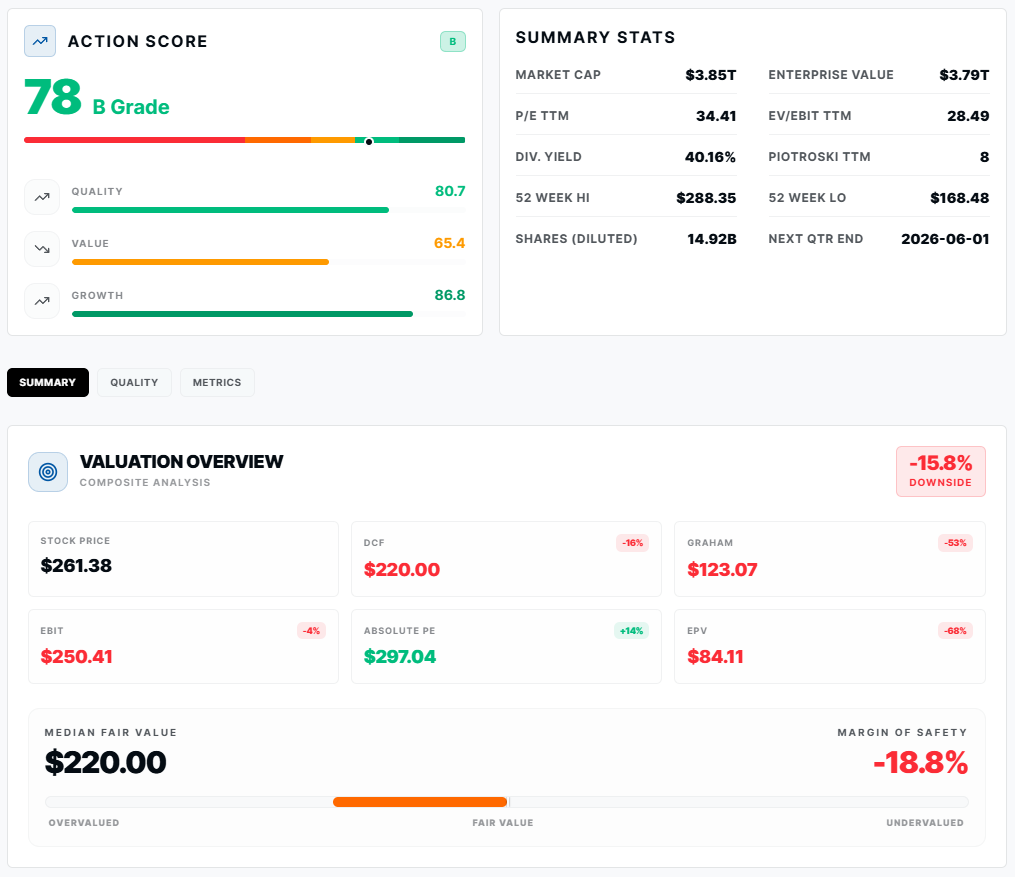

Find Quality Value Stocks

Instantly identify high-quality companies trading with a margin of safety, filtering out the noise to focus on the best investment opportunities.