Does Quality and Value Matter for Juniper Networks?

What You’ll Learn

- Whether Juniper Networks is worth buying

- What the Quality, Value and Growth factors show

- Why it’s important to not get stuck in the numbers

Juniper Networks (JNPR) proves that not all tech companies receive love. It’s a $10B company involved in enterprise networking and IT solutions. Selling, installing, managing and optimizing networks means they compete with names like Cisco (CSCO), HP (HPE) and F5 Networks (FFIV).

But Juniper is the topic of the day as it shows up in my Sleeper Stock screen.

What are Sleeper Stocks?

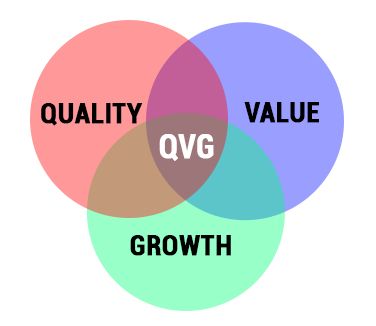

It’s a name I give to find stocks offering Quality + Value. It’s two out of the three core criteria I look for. The three main categories are Quality, Value and Growth.

As the universe of stocks is quite small at the center, I don’t mind venturing out to to find new ideas.

In the image above, Juniper falls in the purple shade between Quality and Value, and the numbers that point to this particular section are as follows:

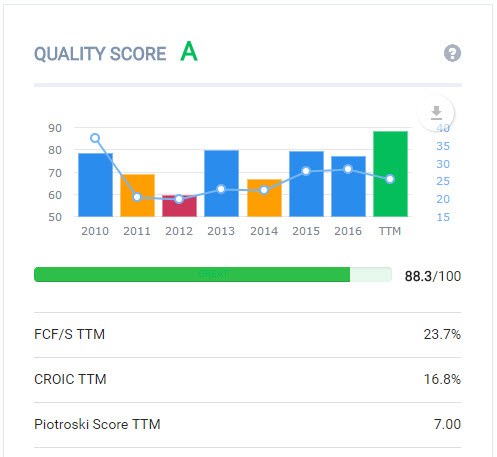

Juniper Quality Score Factors

source: Old School Value Quality Score

FCF/S shows the ability of the company to generate FCF for every dollar of sales. In this case, Juniper is able to transform ever $1 of sales into $0.23 in FCF. Any company that does more than 10% in FCF/S is a cash machine. There has been an increase in debt, but it is easily serviceable with the magnitude of their FCF.

CROIC is a cash version of ROIC. To explain it simply, it measures how well a company is generating cash off its investments. A CROIC of 17% is above average. My rule of thumb is to look for CROIC above 13%.

Juniper Value Factors

For starters, the quick valuation multiple I use to track and rank the value score is determined by P/FCF and EV/EBIT.

P/FCF because it’s hard to go wrong buying companies at a cheap multiple to FCF.

EV/EBIT because it just works. There are plenty of papers and research that show how buying low EV/EBIT stocks outperform. Tobias Carlisle likes to use a modified version of EV/EBITDA in his Acquirer’s Multiple formula. Joel Greenblatt uses the inverse for his magic formula yield.

An EV/EBIT multiple below 11x is my threshold of cheapness.

Other Numbers

By the number so far, you can see the main merit of Juniper is that it is cheap based on FCF. The following numbers again confirm this fact.

- FCF Yield is in double digits

- The earnings yield used in the Magic Formula is also in double digits which is a good area to be in

- ROE is not the highest at 12.5%. This can be improved.

Why Me, God?

In the words of Charlie Munger

When you locate a bargain, you must ask, ‘Why me, God? Why am I the only one who could find this bargain?’ – Charlie Munger

This question is a better version of “Why is this cheap?” and has become a core question on my checklist as I look at stocks. Out of the millions of people investing in the stock market, why do I think this is a bargain?

What am I see that others are not?

Sometimes, it’s something as simple as

- not getting emotional over market fluctuations

- being able to value stocks better than most people

- and buying when others are selling

But most of the time, I don’t know anymore than the person on the other side of the table. I’m just fooling myself if I think I do.

With Juniper, it’s a case where I don’t know.

I don’t know much about data centers, networking, certifications, and the details of the other stuff they do. The best I can do is see what happens when I dig into the numbers and try to figure out the business story from the accounting side.

Where’s the Growth?

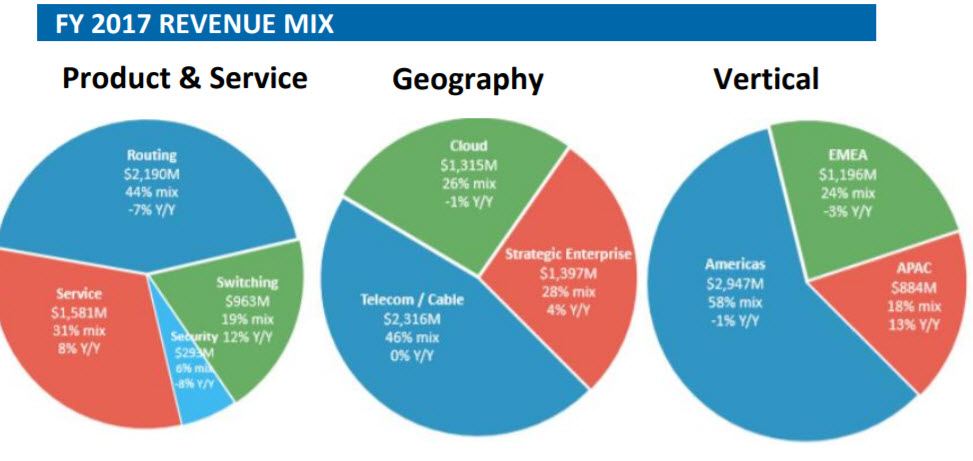

Juniper’s revenue is diversified across 3 main products.

- Routers make up 44% of sales

- Switches is 19%

- Services for planning, building and maintaining data centers is 31%

source: Juniper Investor Presentation

The mix is good, but the YoY numbers are either flat or negative.

46% of sales is also attributed to the networking related side while 26% is for cloud. Considering that we live in an online era where the demand keeps getting higher and higher, it’s surprising to see the cloud section at -1% growth. My viewpoint is limited, but from the presentation I’ve seen about the future of cloud, it’s either Juniper has a sales problem or the presentations that companies make are over hyped.

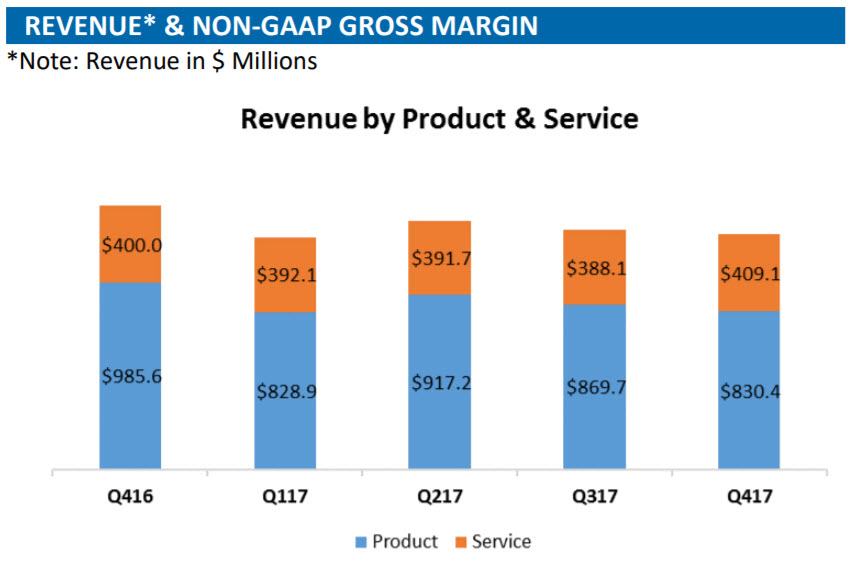

This next chart puts the growth into perspective.

source: Juniper Investor presentation

These are only 5 quarters of data, but with little growth over the past year, it’s not surprising that Juniper’s stock price has lagged. The S&P500 returned 27.6% vs Juniper’s 13.3%.

But it feels like the tide lifted Juniper in this case.

JNPR vs CSCO vs HPE vs VOO | source: Google Finance

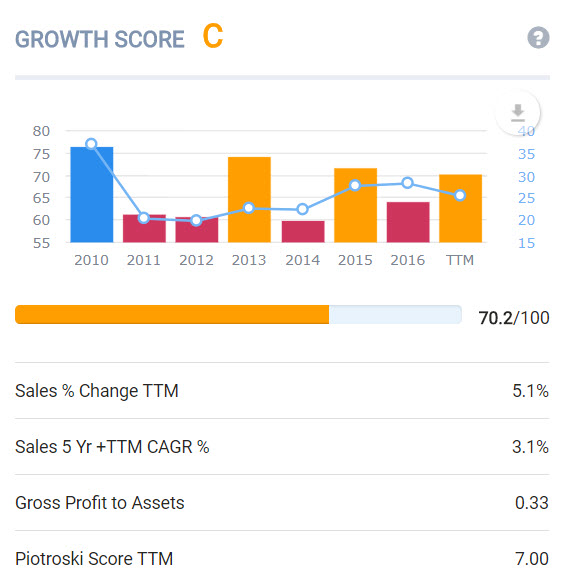

Juniper gets a C grade in the growth department with Old School Value, but that’s only thanks to a high Piotroski score which means the accounting numbers and fundamentals are good.

If the Piotroski score was below the 7 threshold, it would be a D.

source: Old School Value Growth Score

When it comes down to it, growth is not a strong point for Juniper. The other factor is that for every dollar of assets, Juniper generates $0.33 of profit. Cisco is worse with a GPA of 0.23 and HPE is the worst with a GPA of 0.17.

Overall, the businesses involved in this industry as a whole are run inefficiently. Lots of fat.

For Juniper to get a jumpstart, they need a catalyst. Some way to come up with killer products or get leaner.

Therein lies the problem.

I have the darnedest clue of what they can do. I don’t understand the details of the business to get in firing range of figuring out whether there is upside. The hardest part about trying to understand these enterprise businesses because I don’t know what I don’t know.

- What growth initiatives exist that will kick sales to another level?

- How are sales people being incentivized to really crush it and meet sales goals?

- What areas of the business can be optimized or expanded?

- How can efficiency and ROI be improved?

I don’t know the answers to any of these questions. I’d bet it’s the same reason why investors are not excited about the company. They can’t speculate about what the next big product. There’s no buzz.

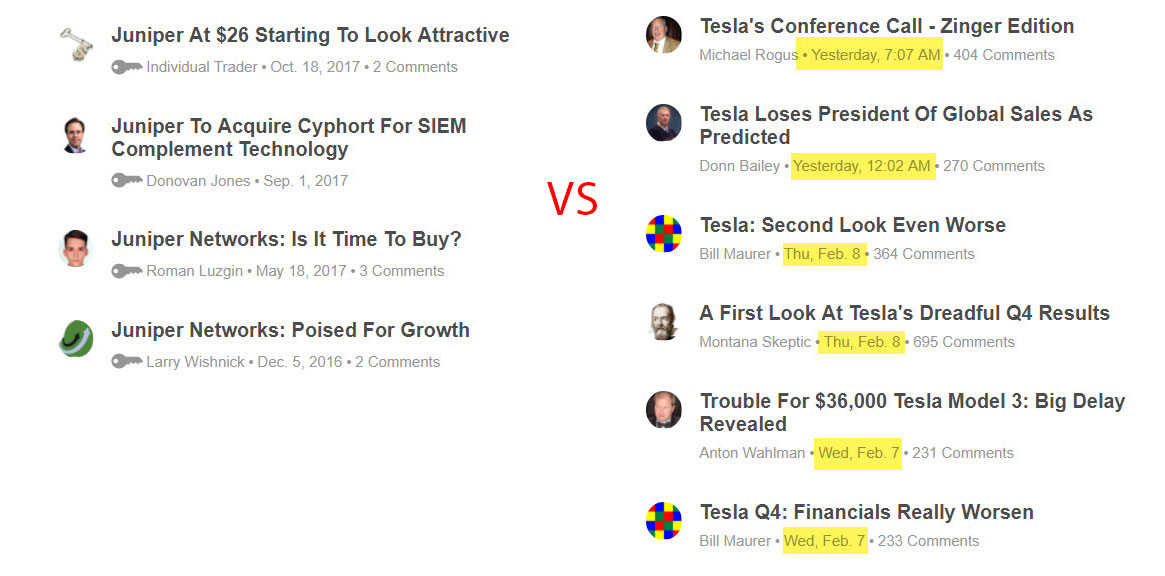

It’s not often you see a $10B market cap company totally off the radar with investors. Only 3 articles were written about Juniper in all of 2017, versus the several that come up daily for hot stocks like TSLA.

The number of articles written about a company is an easy indicator of investor sentiment and how easy the company is to understand.

No love for Juniper. | source: Seeking Alpha

Will This Sleeper Stock Wake Up?

I knew going in that Juniper had low growth prospects. I searched for Q+V after all. You can see why I call these types of companies “Sleeper Stocks”.

But for sleeper stocks to do well, they need to wake up. In Juniper’s case, I don’t see that happening easily and for that reason, I have no position.

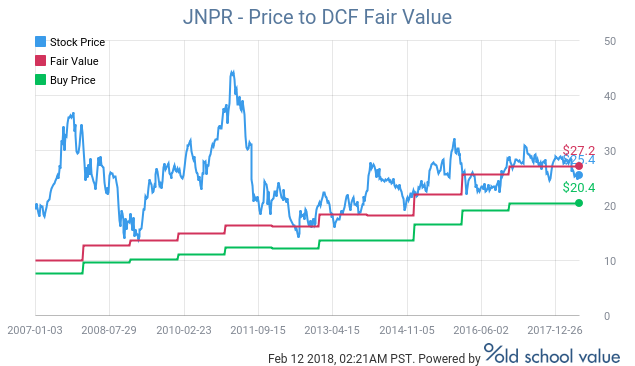

DCF Fair Value for JNPR

Disclosure

No position.